PBSA Series: What the listed market already knows

Private capital tends to follow public capital with a lag. The handful of listed student-housing names left in Europe are pricing the next leg of the PBSA cycle now — and once you decode the appraisal lag, the read for European and Spanish private assets is largely determined.

Across this series we have argued the Spanish PBSA case from the ground up: a national provision rate near 7% against structural demand, returns that are earned at the sub-market rather than the national average, and an institutional development model built for scale on the outskirts that leaves the central premium segment structurally unoccupied. Each of those arguments is built on private-market evidence — supply counts, enrolment data, appraisals and closed transactions.

Private-market evidence has one defect: it is slow. Appraised values are smoothed, reported quarterly, and anchored to comparable transactions that closed months earlier. By the time a private valuation moves, the information that moved it is old. There is, however, a faster instrument measuring the same buildings, the same tenants and the same rental cash flows — repriced every single trading day. That instrument is the listed student-housing sector. This piece reads it, and translates what it is saying into the Spanish private market.

I. WHY LISTED LEADS PRIVATE

A listed REIT and a private fund holding identical buildings will report wildly different short-run returns. The rolling one-year correlation between listed real estate (“RE”) and the private ODCE index has been only about 16% since 1989.1 Read naïvely, that looks like two different asset classes. It is not. It is one asset class observed through two measurement systems.

Listed equity is marked to market continuously: every revision to expected rents, financing costs and exit yields is priced into the share that afternoon. Private RE is marked to appraisal: valuers move deliberately, lag transaction evidence, and smooth across periods. Correct the private series for that smoothing and the relationship resolves — the lagged correlation over 25 years is approximately 0.90.1 Same asset, same fundamentals, different clock.

The order of operations is what matters. Listed prices incorporate new information first; private appraisals catch up over the following two to four quarters. Listed RE tends to lead private in both downturns and recoveries.1 Interestingly, listed REITs have outperformed the private ODCE index by roughly 40% since the third quarter of 2022 as the public market re-rated ahead of private marks.1 This is consistent with what Cohen & Steers find specifically in Europe: listed European REITs bottomed and re-rated while the INREV index of European private real estate funds continued to decline, and they put the typical lead at 12 to 18 months in both selloffs and recoveries.1 The US relationship is the better-documented one (the 0.90 lag-adjusted correlation is a US ODCE figure), but the same lead-lag dynamic is observed in Europe, which is the relevant read for Spanish private assets.

Bottom line: Listed student housing is not a different market from Spanish private PBSA — it is the same market reporting earlier. The job is to read the listed signal and discount it back into a private underwrite, not to dismiss it as a separate asset class.

II. THE LISTED UNIVERSE IS VANISHING – AND THAT'S THE FIRST SIGNAL

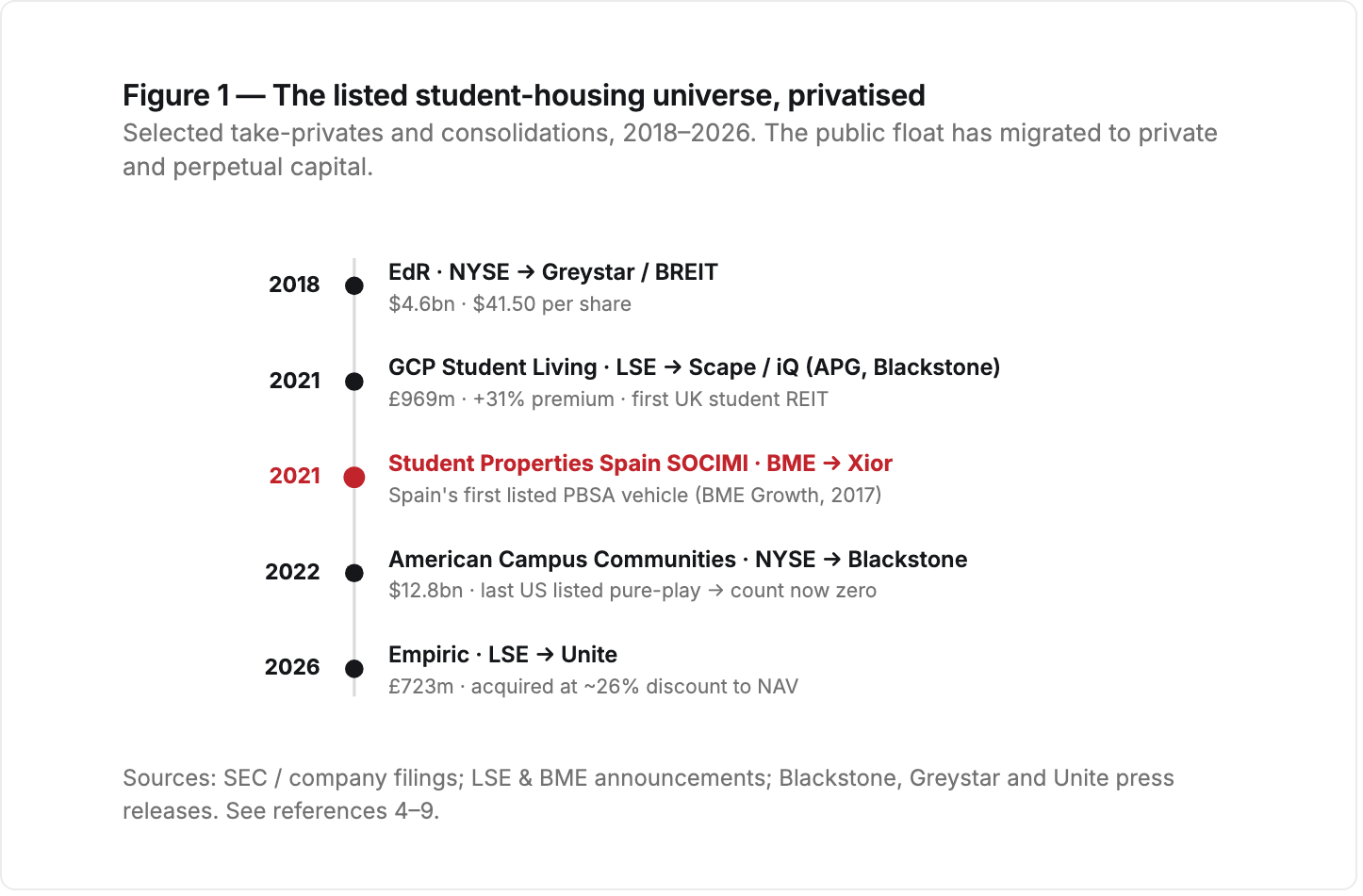

The most important thing the listed PBSA market has done over the past eight years is shrink. One by one, the listed pure-plays have been bought by private and perpetual capital, almost always at a premium to the undisturbed share price and frequently at a discount to stated NAV.

i) United States — the pure-play count is now zero

Education Realty Trust (EdR), NYSE-listed, was acquired by a Greystar-led fund for $4.6bn ($41.50/share) in September 2018, with a BREIT/Greystar venture taking a $1.2bn slice of the portfolio.4 That left American Campus Communities (ACC) as the last listed US pure-play — until Blackstone took it private for $12.8bn ($65.47/share) in August 2022, citing “strong historical performance” and a “shortage of quality housing supply.”6 After ACC, the number of listed US pure-play student-housing REITs is zero. The entire sector concluded it was worth more in private hands than the public market would pay.

ii) United Kingdom — consolidation down to one

GCP Student Living, the first UK student-accommodation REIT, was taken private in 2021 by a Scape/iQ consortium backed by APG and Blackstone for £969m, a 31% premium to the undisturbed price.5 Then in January 2026 Unite completed its £723m acquisition of Empiric Student Property (c. £156k per bed on full portfolio value) — removing the LSE's last mid-cap PBSA name and leaving Unite as effectively the only listed UK pure-play of scale.7 Crucially, Empiric was acquired at an average 22% discount to its EPRA NTA over the prior year: a strategic buyer arbitraging a public-market discount on a private company.9

iii) Spain — the proof point on a Spanish ticker

This is the read closest to home. Student Properties Spain SOCIMI (BME: YSPS) was the first specialised student-housing vehicle listed in Spain (albeit relatively small with 725 beds), on BME Growth since 2017. Its portfolio was anchored by the central-Madrid Retiro asset (which now sits inside Xior's Spanish book — see Section IV). It was taken over in 2021 by Xior Student Housing, the pan-European operator, for €58.5m and delisted, with Xior describing the move as validating the Spanish market “as a resilient segment with high growth potential.”8

Bottom line: When an entire listed sub-sector is bought in and delisted at premiums to share price but discounts to NAV, the market is making a statement: private buyers value the cash flows more highly than public equity will, and they are willing to pay to control them. For Spanish PBSA that statement was already made — on the BME — in 2021.

III. WHAT THE SURVIVORS ARE TELLING US

Two listed names still report against PBSA fundamentals frequently enough to be useful instruments: Xior (Euronext Brussels), the pan-European operator with direct Spanish exposure, and Unite (LSE), now the UK pure-play of scale. Xior is the closest listed proxy a Spanish underwriter has to a mark-to-market read on their own market.

i) Xior — the Spanish read is still hot, but watch the spread

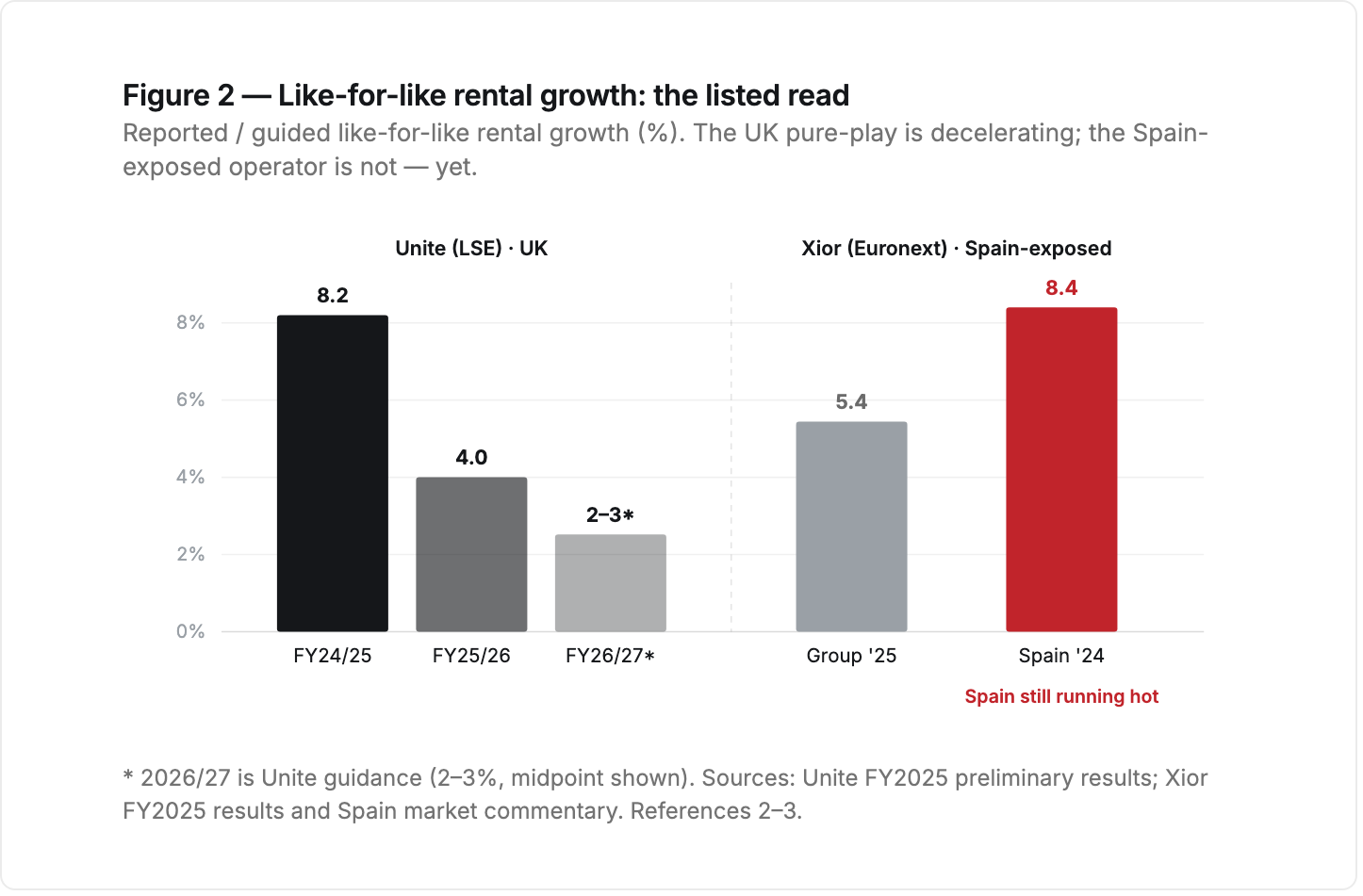

Xior delivered 5.4% group like-for-like rental growth in 2025 on a ~€3.6bn portfolio, ahead of guidance and well ahead of inflation.3 Within that, Spain remains its hottest market: 98% academic-year occupancy (both Madrid assets 100% let), rents up 8.4% in 2024, and studios above €1,200/month in Madrid and Barcelona (more on Xior in Section IV).3,12

ii) Unite — the rental-growth step-down

Unite's reported like-for-like rental growth has decelerated in clean, consecutive steps: 8.2% in the 2024/25 academic year, 4.0% for 2025/26, and guidance of 2–3% for 2026/27, with occupancy easing from 97.5% to 95.2% and guided to 93–96%. The wider FY2025 numbers are those of a mature, conservatively-financed platform: a £6.6bn portfolio, LTV of 27% (up from 24%), net debt to EBITDA of 6.0x, a see-through net initial yield of 5.2% (out 11bps on the year), cost of debt rising to 4.3% in 2026 and 4.5% in 2027, a 37.7p dividend held flat, and a total accounting return of just 2.1% after a 2% fall in EPRA NTA to 955p.2 Management attributes the softening to changing student behaviour at lower-ranked universities and slower lease-up after large projects — a quality-of-demand story this series has made repeatedly at the sub-market level. Unite is reporting in real time that the demand bifurcation is structural, and that the UK market is further through the rental cycle which Spain is still early in.

Bottom line: 1) Spanish PBSA is still much earlier in its rental cycle than the UK — the deceleration visible in Unite has not yet arrived in Xior's Spanish book. 2) The gap between Xior's Spanish growth and Unite's UK growth may well be precisely the spread between the UK and Spain: the UK is showing Spain its possible trajectory c. 5–10 years out. However, considering the beds shortage in Spain and the increasing net number of students, the Spanish PBSA market may well still be growing ten years in.

IV. INSIDE XIOR'S SPANISH BOOK

Key points from reading Xior's FY2025 annual report:

i) The group frame

€3.56bn of property across 22k units in eight countries; 98% average occupancy; like-for-like rental growth of 5.4% against a 5% guide; EPRA EPS of €2.22, with a €2.30 guide for 2026 — the first earnings growth after three flat, deleveraging years; loan-to-value below 50% for the first time; average cost of debt 3.1% (well inside Unite's 4.3% and a function of EU’s cost of debt); EPRA net initial yield 4.8%.12 The share closed 2025 at €28.95 against an EPRA NTA of €38.67 — a 25% discount.12

The single most striking number is the last one: a portfolio that is effectively full, compounding rents above inflation, with leverage falling and earnings turning up — priced by the public market at a quarter below what its own auditors say it is worth.

The earlier-mentioned pattern from Section II persists in miniature: a platform compounding rents above inflation, effectively full, and priced by public equity at three-quarters of its appraised book.

ii) The Spanish book

10 standing assets, 2.5k units, six cities (Madrid, Barcelona, Zaragoza, Granada, Málaga, Seville). Fair value €417m, up from €385m a year earlier on an unchanged unit count, representing an 8% yoy increase. The Iberia segment grew net rental income 12.7% and posted a +€42m revaluation — the only geography in the group with a material positive mark in 2025 (Belgium and the Netherlands were both written down).12 Spain's gross valuation yield: 5.13% (the tightest of Xior's eight countries).

The valuers' inputs are the most useful disclosure in the document: weighted-average rent per room €965/month all-in (range €373–1,955 — Spanish rents are booked inclusive of services), academic-year occupancy 98%, summer occupancy 59% (from 50% a year earlier — the dual-season, summer-ADR revenue layer 404’s PBSA series flagged in Part 3 now showing up in audited numbers), and a DCF discount rate of 7.8%, wider than last year's 7.5%.12 The Spanish portfolio also achieves the highest rents of any country Xior operates in — ahead of the Netherlands, Belgium and Denmark — largely because Spanish residences bundle more services (cleaning, food) into the rent.

iii) Asset by asset — Madrid only (no disclosures on Barcelona assets)

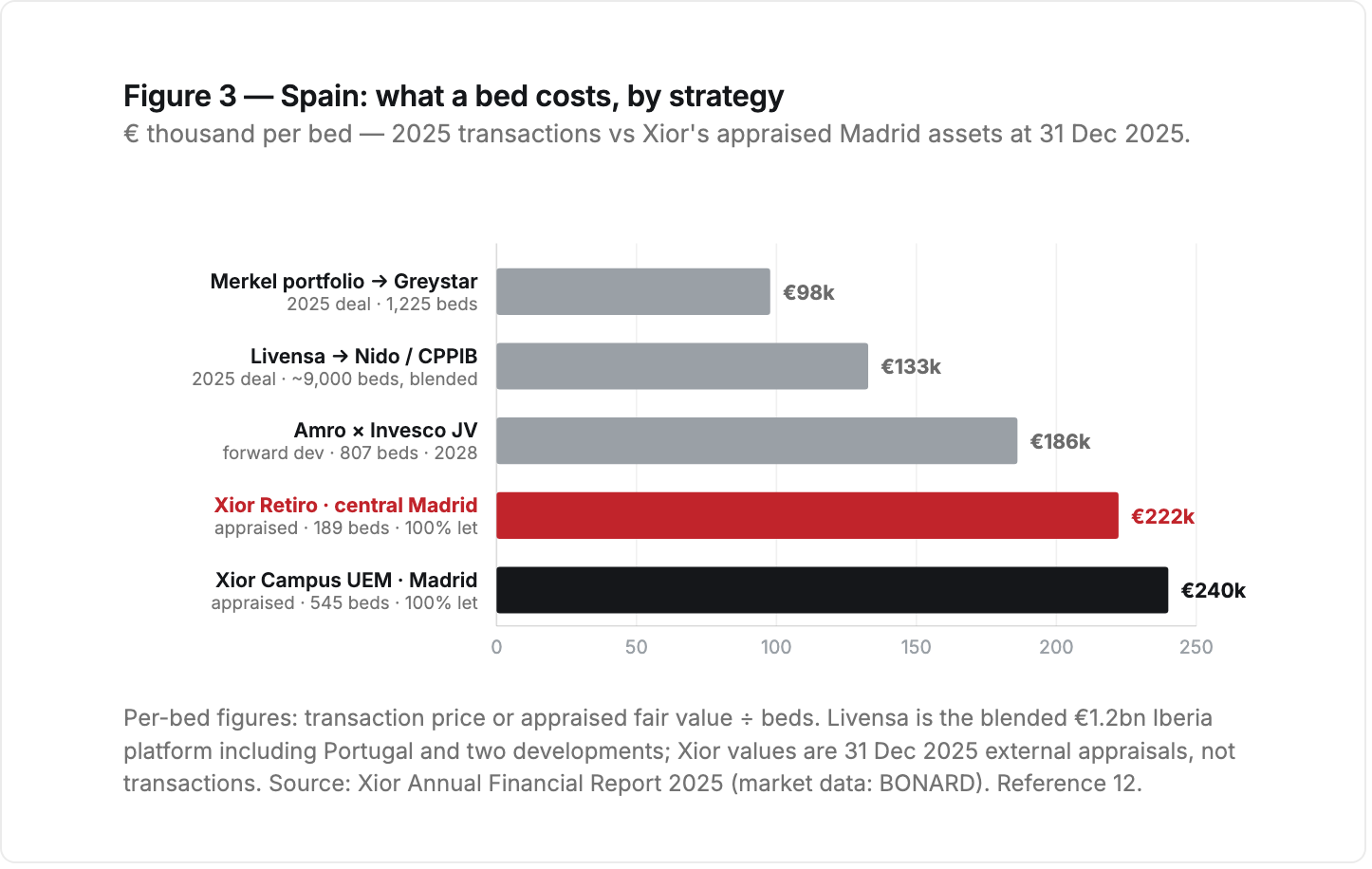

Campus UEM (Villaviciosa de Odón, on the Universidad Europea de Madrid campus). Built 2016; 490 units / 545 beds across 16.5k sqm; 100% financial occupancy; estimated rental value €9.6m; fair value €131m — roughly €240k per bed.

Having looked at Xior's website, for AY 26/27, all single rooms (except for the most basic room - Individual Confort) are booked out and the available Individual Confort starts from €2,050 a month for the most basic room, which itself is a 14 sqm with basic finishes and a 100cm bed. It shows how much demand appetite and pricing power there are for premium residences in right locations. Furthermore, Xior Campus UEM is the largest asset in Xior's entire eight-country book by rent.12 The private-university campus model at full scale.

Retiro (central Madrid — the asset that came with the Student Properties Spain SOCIMI take-private of Section II). Built 2018; 146 units / 189 beds across 5,840 sqm; 100% occupancy; estimated rental value €3.4m; fair value €42m — €288k per unit, €222k per bed.12 This is close to the product that Cuatro Urban Living aims to deliver: central, ~100 beds, premium product, full occupancy.

With regards to the Barcelona assets, there is no per-asset disclosure, except for three assets, 397 units (Gràcia, Collblanc and Diagonal Besòs) and a city provision rate of just 7.7%.12

Bottom line: Xior's audited book proves the asset works — central Madrid PBSA valued at €222k+ per bed, fully let — even as the listed wrapper trades 25% below NAV. The product is validated; the central premium segment is still unbought.

V. READING IT ACROSS SPANISH PBSA

Translating the listed signal into a Spanish private underwrite produces four concrete adjustments rather than vague optimism.

1. Quality of demand bifurcates first in the listed data. Unite's occupancy softness is concentrated at lower-ranked universities. This is the sub-market thesis of Part 2, confirmed by a mark-to-market instrument: in Spain, hold the underwrite to prime, supply-constrained central districts and resist pricing peripheral, lower-tier-university stock as if it were core.2

2. Rental growth: elevated now, converging later. Even the hottest listed book is guided down: Xior grew 5.4% like-for-like in 2025 and guides “at least 4%” for 2026, while Unite has stepped 8.2% → 4.0% → 2–3%.212 Underwrite strong near-term Spanish growth, model convergence toward low single digits over the hold — and treat the longer, shortage-driven runway of Section III as upside, not base case.

3. Value growth: underwrite rents, not yield compression. Xior's Spanish marks rose 8% in 2025 while its valuers widened the DCF discount rate to 7.8% and the country yield marker sits at 5.1% — already the tightest in its book.12 The market is paying for income, not multiple. Build the exit off today's yield and let compression be optionality.

4. Exit liquidity is private — and it is now priced. There is no listed exit: Spain's one listed vehicle was absorbed, and the public market prices the survivors at 25%+ discounts to NAV. The buyers are platforms and perpetual capital, and 2025 printed the ladder: ~€98k per bed for a regional operational portfolio, ~€133k blended for the €1.2bn Livensa platform, ~€186k for forward development, and ~€222k appraised for central Madrid product (Xior Retiro) rising to ~€240k for the premium campus asset (Campus UEM) — the levels set out in Section IV.12

Bottom line: The listed market gives Spanish PBSA a head start: when growth slows, where demand splits, what the exit is worth per bed, and who buys at the end.

VI. 404 VIEW

Xior's audited Spanish book shows what sits underneath the Spanish curve: full assets, rent-led revaluations against a widening discount rate, the tightest yields of its eight countries.

Our positioning follows this directly. The one disclosed Spanish asset in Madrid that resembles the Cuatro underwrite — 146 central-Madrid units — is 100% let and appraised at €222k per unit, while no institutional platform, Xior included, buys below its ~150-unit operating floor. We underwrite Spanish central, supply-constrained, quality-of-demand-protected assets — the Post 3 of this series identified as structurally unoccupied — to a private or strategic exit, at the per-bed levels the 2025 market has now printed, with deliberately conservative terminal growth and exit yields. The listed market has told us where this cycle is heading, who will be buying at the end of it, and at what price. We are underwriting to that buyer, in that segment, before the private marks catch up.

We consciously decided to focus on best-in-class assets in A locations to occupy the country’s vacant premium brand positioning. As the market matures and more investment is happening in the Spanish PBSA sector, we want an A-class product that outcompetes a large PBSA scheme on most characteristics other than sheer amenity count, protected by a geographical moat (a good location itself) and a clear boutique premium position. The UK market is already showing why this matters. In Unite's 2025 results, 19 of its 22 cities averaged 97% occupancy, while the entire shortfall was concentrated in three lower-tariff regional cities — Leicester, Nottingham and Sheffield — where new supply met softer demand. Unite's strategic response was to dispose of 3,700 beds in regional markets and reinvest £1.3bn into assets serving the strongest universities, lifting its high-tariff alignment from 67% toward a targeted 80%. The most mature institutional operator in European PBSA is, in other words, actively selling the periphery and buying quality and location. That is the bifurcation our PBSA series has argued from the start, now visible in a FTSE 100 operator's capital allocation.

About 404 Capital

404 Capital ("404") is a London-based real estate investment firm that identifies supply-starved sectors and builds operational real estate platforms from the ground up. Our first platform is Cuatro Living ("Cuatro"). Cuatro is the next generation of student and young-professional living in Spain — boutique hospitality, residential at heart, with PBSA as the primary product and flex residences as a secondary one. Design-led, boutique-scale residences (typically 70–120 beds) with high-quality finishes and amenities, situated near educational institutions and in well-connected locations across Spain's leading university cities. Operated in-house by Cuatro with a tech-forward operating model.

Disclaimer

For professional investors only; not intended for retail clients. 404 Capital Ltd is not authorised or regulated by the FCA. This material is for discussion purposes only and does not constitute investment, legal or tax advice. Operator descriptions reflect publicly available sources and a property-level dataset compiled by 404 Capital; capital structure descriptions reflect public disclosures and trade press coverage and may not capture the full ownership structure or most recent changes. Investors should conduct their own due diligence on any specific platform or asset.

References

1. Cohen & Steers, “Exploring the lead-lag relationship of listed and private real estate”; CEM Benchmarking / Nareit lag-adjusted correlation study. cohenandsteers.com, reit.com

2. The Unite Group plc, Preliminary results for the year ended 31 December 2025 (24 Feb 2026). unitegroup.com

3. Xior Student Housing NV, FY2025 results and Spain market commentary. xior.prezly.com

4. Greystar, “Greystar Announces Completion of $4.6 Billion EdR Acquisition” (Sept 2018). prnewswire.com

5. IPE Real Assets, “APG, Blackstone, Scape to buy FTSE 250-listed GCP Student Living” (2021). realassets.ipe.com

6. Blackstone, “Blackstone Funds Complete $13 Billion Acquisition of American Campus Communities” (Aug 2022). blackstone.com

7. The Unite Group plc, “Unite Group completes purchase of Empiric Student Property” (Jan 2026). unitegroup.com

8. AltamarCAM Partners, “Student Properties Spain SOCIMI announces a takeover bid from Xior Student Housing.” altamarcam.com

9. Investing.com, “Unite reports 2% NAV drop, flags softer FY26 rental growth” — Empiric traded at ~26% average discount to EPRA NTA pre-acquisition. investing.com

10. The Unite Group plc (UTG.L) market price. marketbeat.com, unitegroup.com

11. Savills, “European Purpose-Built Student Accommodation Investment Barometer Report — 2025.” savills.com

12. Xior Student Housing NV, Annual Financial Report 2025 — audited FY25 accounts; property report market data: BONARD (2026); external valuations: CBRE and Cushman & Wakefield. xior.be